Roth IRA: The Complete Guide ({{YEAR}})

Everything you need to know about how Roth IRAs actually work — contributions, withdrawals, the 5-year rules (yes, plural), and the details most people get wrong.

What Is a Roth IRA?

A Roth IRA is an individual retirement account funded with after-tax dollars. You contribute money you've already paid taxes on. It grows tax-free. And when you take it out in retirement, you pay nothing.

That's the deal. You pay the tax now. The IRS leaves you alone later.

Like a Traditional IRA, it's a container, not an investment. Inside the Roth, you can hold stocks, bonds, mutual funds, ETFs, CDs, or cash. The Roth is the wrapper. What goes inside is your choice.

The big difference from a Traditional IRA: no tax deduction going in, no tax bill coming out. No Required Minimum Distributions during your lifetime either. The money can sit there and grow as long as you want.

There's a catch. Not everyone can contribute to a Roth IRA. There are income limits.

Who Can Contribute?

Two requirements.

You need earned income. Same as a Traditional IRA. W-2 wages, self-employment income, commissions, tips. Investment income and rental income don't count.

Your income must be below the Roth IRA limits. Unlike a Traditional IRA, which anyone with earned income can contribute to, the Roth has income phase-outs that can reduce or eliminate your ability to contribute.

There is no age limit. A 16-year-old with a summer job can open a Roth IRA. An 85-year-old with consulting income can contribute. Age doesn't matter. Earned income and MAGI do.

Income Phase-Outs for {{YEAR}}

Your ability to contribute depends on your Modified Adjusted Gross Income (MAGI) and filing status.

| Filing Status | Full Contribution | Reduced Contribution | No Contribution |

|---|---|---|---|

| Single / Head of Household | MAGI < $153,000 | $153,000 – $168,000 | Above $168,000 |

| Married Filing Jointly | MAGI < $242,000 | $242,000 – $252,000 | Above $252,000 |

| Married Filing Separately | N/A | $0 – $10,000 | Above $10,000 |

The Spousal IRA Exception

Same as with a Traditional IRA. If you're married and file jointly, a non-working spouse can contribute to their own Roth IRA based on the working spouse's earned income — see our Spousal IRA guide for the full rules. The combined household MAGI still has to fall below the phase-out thresholds.

What If You're Over the Income Limit?

You can't contribute directly. But there's a workaround called the Backdoor Roth IRA. You contribute to a non-deductible Traditional IRA (no income limit for contributions), then convert it to a Roth. Legal and widely used.

{{YEAR}} Contribution Limits

| Age | Annual Limit |

|---|---|

| Under 50 | $7,500 |

| 50 or older | $8,600 (includes $1,100 catch-up) |

These are the same limits as a Traditional IRA because they're shared. The $7,500 limit is the combined total across all your Traditional and Roth IRAs. You can split it any way you want, but the total can't exceed $7,500 ($8,600 if you're 50+).

You also can't contribute more than your earned income. Made $4,000? That's your max, regardless of the IRS limit.

This matters for the 5-year rule too. A contribution made in February 2027 for the 2026 tax year starts the 5-year clock on January 1, 2026 — nearly a full year earlier than the calendar date suggests.

If you contribute more than the limit, the IRS charges a 6% penalty on the excess for every year it remains in the account. Calculate the exact corrective withdrawal →

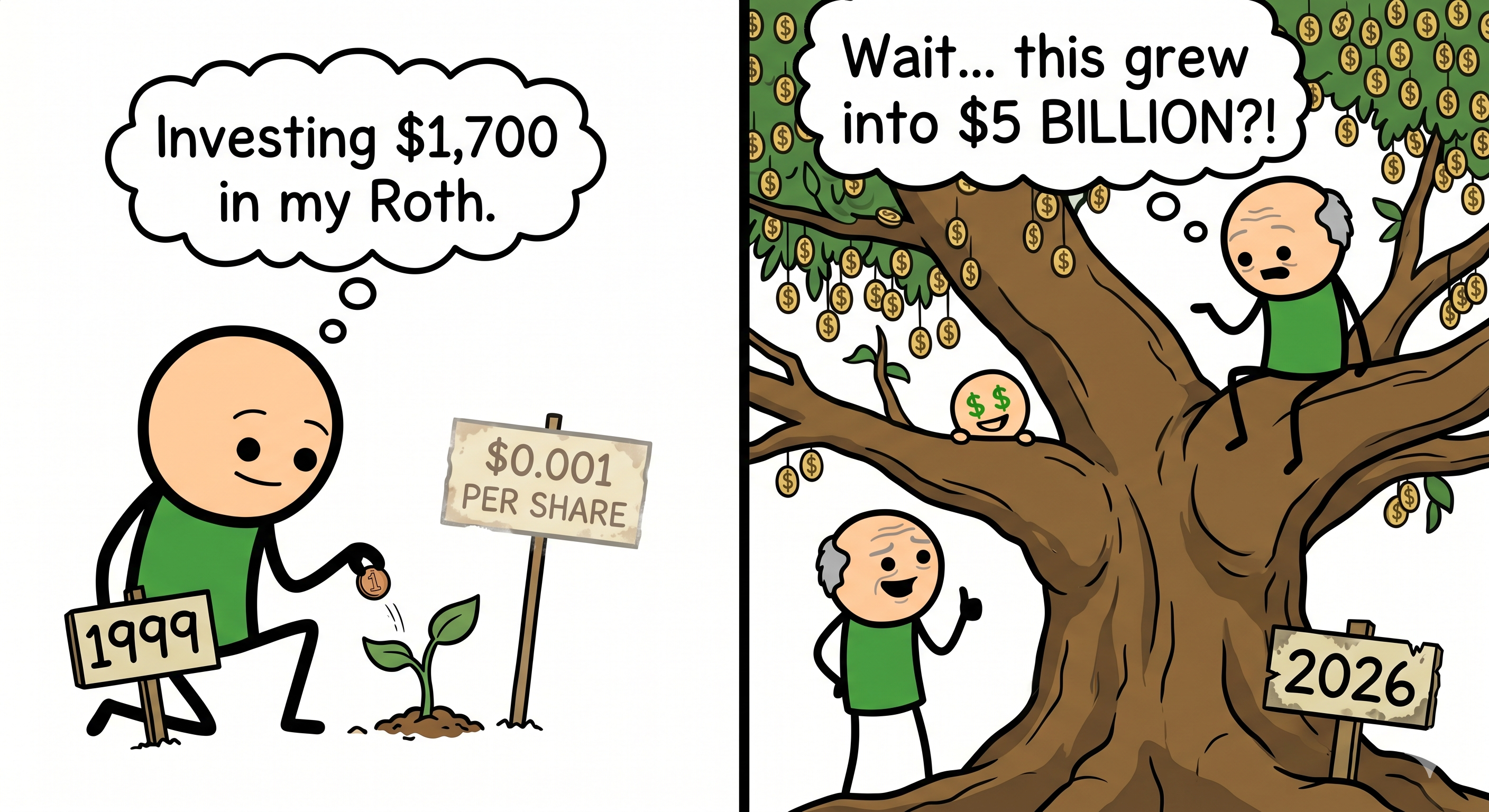

While most people are focused on the $7,000 contribution limit, Peter Thiel (co-founder of PayPal) managed to grow a Roth IRA to $5 billion. In 1999, he used $1,700 in his Roth to buy 1.7 million shares of PayPal when it was still a private startup, valued at $0.001 per share. Because the shares were private and the valuation was considered fair at the time, it was perfectly legal. He put the world's greatest lottery ticket inside the world's best tax shelter. When he turns 59½, he can withdraw all $5 billion without paying a cent in federal income tax. Congress has discussed closing the loophole that allows private-company stock at artificially low valuations inside retirement accounts, but so far, no legislation has passed. The contribution limit exists to prevent most people from doing what Thiel did. It just didn't prevent Thiel.

How Withdrawals Work

This is where Roth IRAs get their reputation, and where most of the confusion lives. The withdrawal rules depend on what you're taking out and when.

The Ordering Rules

The IRS doesn't let you choose which dollars come out first. Roth IRA distributions follow a specific order:

- Regular contributions come out first. Always tax-free. Always penalty-free. Regardless of your age or how long the account has been open. You already paid tax on this money. The IRS has no further claim on it.

- Converted and rolled-over amounts come out second. On a first-in, first-out basis. The taxable portion of each conversion comes out before the non-taxable portion. These may be subject to the 10% penalty if withdrawn within 5 years of the conversion and you're under 59½.

- Earnings come out last. This is where the 5-year rule and the age requirement matter most. Earnings can be tax-free and penalty-free, but only if the withdrawal qualifies.

Qualified Distributions

A qualified distribution from a Roth IRA is completely tax-free and penalty-free. To qualify, two conditions must be met:

Condition 1: The 5-year rule. Your first contribution to any Roth IRA must have been made at least 5 tax years ago.

Condition 2: One of these must also be true:

- You're age 59½ or older

- You're disabled (permanent and total, as defined by the IRS)

- The distribution is made to a beneficiary after your death

- The distribution is for a first-time home purchase (up to $10,000 lifetime limit)

Meet both conditions and everything comes out tax-free — contributions, conversions, and earnings. All of it.

Non-Qualified Distributions

If you don't meet both conditions, the tax treatment depends on which layer of money you're withdrawing (see the ordering rules above).

- Contributions: always tax-free and penalty-free.

- Conversions: tax-free (you already paid tax on the conversion), but may be subject to the 10% penalty if withdrawn within 5 years and you're under 59½.

- Earnings: taxable as ordinary income, plus the 10% penalty if you're under 59½, unless an exception applies.

The 5-Year Rules

Yes, rules. Plural. There are two separate 5-year rules for Roth IRAs, and confusing them is one of the most common mistakes in retirement planning.

5-Year Rule #1: The Earnings Clock

This determines when your earnings qualify for tax-free withdrawal. The clock starts on January 1 of the tax year of your first contribution to any Roth IRA.

- It only starts once. Your first Roth IRA contribution sets the clock for all your Roth IRAs. It doesn't restart when you open a new Roth or make additional contributions.

- It backdates to January 1. If you make your first Roth contribution in December 2026, the clock starts January 1, 2026. If you make it in March 2027 for the 2026 tax year, the clock also starts January 1, 2026.

- Once you hit the 5-year mark and turn 59½, every dollar in every Roth IRA is available tax-free.

5-Year Rule #2: The Conversion Clock

This applies specifically to money you've converted from a Traditional IRA (or other pre-tax retirement account) to a Roth IRA. It's designed to prevent people from using conversions to dodge the early withdrawal penalty.

Each conversion has its own separate 5-year clock. The clock starts on January 1 of the year you made the conversion. If you convert in December 2026, the clock started January 1, 2026. If you convert again in 2027, that conversion gets its own clock starting January 1, 2027.

If you withdraw converted amounts within the 5-year window and you're under 59½, the 10% early withdrawal penalty applies to the taxable portion of the conversion. (You already paid income tax on the conversion. The penalty is on top of that.)

Once you turn 59½, the conversion clock becomes irrelevant. You're past the penalty age. The only 5-year rule that still matters at that point is the earnings clock.

How They Work Together

| Situation | Tax & Penalty Treatment |

|---|---|

| Age 59½+ and first Roth contribution was 5+ years ago | Everything is tax-free and penalty-free |

| Age 59½+ but first Roth contribution was less than 5 years ago | Contributions and conversions tax-free; earnings taxable (no penalty) |

| Under 59½ and conversion was less than 5 years ago | Contributions tax-free; conversion amounts may trigger 10% penalty; earnings taxable + penalty |

The ordering rules protect you in most situations because contributions come out first. But if you've done large conversions and you're under 59½, be careful about the conversion clock.

No Required Minimum Distributions

This is one of the biggest advantages of a Roth IRA over a Traditional IRA.

There are no Required Minimum Distributions from a Roth IRA during your lifetime. None. The money can sit in the account and grow tax-free for as long as you live.

This makes the Roth IRA a powerful estate planning tool. You can leave the entire balance to your beneficiaries. They'll eventually have to take distributions (the 10-year rule under the SECURE Act applies to most non-spouse beneficiaries), but those distributions are generally tax-free as long as the original owner's 5-year rule was satisfied.

Your spouse can roll your Roth IRA into their own Roth IRA after your death and continue the tax-free growth with no RMDs during their lifetime either.

Roth Conversions

You can convert money from a Traditional IRA, SEP IRA, SIMPLE IRA, or former employer plan (like a 401(k)) into a Roth IRA. The converted amount is added to your taxable income for the year. There is no limit on how much you can convert.

Why would you voluntarily pay taxes now? Because you're buying tax-free growth and tax-free withdrawals forever. If you expect your tax rate to be the same or higher in retirement, paying the bill now can save you significantly over time.

Conversions make the most sense when your income is temporarily lower than usual — transition years between jobs, early retirement before Social Security kicks in, or years with large deductions.

The Pro-Rata Rule

If you have both pre-tax and after-tax (non-deductible) money across your Traditional IRAs, you can't cherry-pick which dollars to convert. The IRS treats all your Traditional, SEP, and SIMPLE IRA balances as one pool and applies the pro-rata rule. The ratio of pre-tax to after-tax money determines how much of the conversion is taxable, calculated on Form 8606.

This is the rule that makes the Backdoor Roth IRA strategy complicated for anyone with existing pre-tax IRA balances.

Want to see the pro-rata math on your exact numbers before you convert? Run your numbers with the Pro-Rata Calculator →

We built a free tool that walks through the tax comparison: Roth vs. Traditional Comparison Tool →

Exceptions to the 10% Early Withdrawal Penalty

These exceptions apply when you're under 59½ and withdrawing earnings or recent conversion amounts. They waive the 10% penalty. They do not make earnings tax-free — for that, the distribution must be qualified (5-year rule met and qualifying event).

Remember: contributions are always available without penalty or tax, regardless of these exceptions. These rules only apply to the earnings and conversion layers.

- Substantially Equal Periodic Payments (SEPP/72(t)): A series of substantially equal payments based on your life expectancy. Must continue for 5 years or until you turn 59½, whichever is later. Modify the schedule early and the IRS retroactively applies the penalty to every distribution.

- Disability: Permanent and total disability as defined by the IRS.

- Death: Beneficiaries receive distributions without the 10% penalty.

- Unreimbursed medical expenses: Expenses exceeding 7.5% of your adjusted gross income.

- Health insurance while unemployed: Must have received unemployment compensation for at least 12 consecutive weeks.

- First-time home purchase: Up to $10,000 lifetime limit. Funds must be used within 120 days. "First-time" means you haven't owned a home in the previous two years.

- Higher education expenses: Tuition, fees, books, supplies, and room and board (if enrolled at least half-time) for you, your spouse, children, or grandchildren.

- Birth or adoption: Up to $5,000 per parent per event. Added by the SECURE Act.

- IRS levy: If the IRS levies your IRA to pay back taxes, the penalty doesn't apply.

- Qualified reservist distributions: National Guard or reserves members called to active duty for 180+ days.

- Qualified disaster distributions: Up to $22,000 per federally declared disaster.

- Domestic abuse: Up to $10,000 (adjusted for inflation) or 50% of the account balance, whichever is less.

- Emergency personal expense: One withdrawal up to $1,000 per calendar year for an unforeseeable financial need.

Rollovers and Transfers

Roth IRA to Roth IRA

Direct transfers between Roth IRAs are unlimited. No tax, no penalty, no annual limit. The 5-year clock carries over from your original Roth IRA.

Roth 401(k) to Roth IRA

When you leave an employer, you can roll your Roth 401(k) into a Roth IRA. The money maintains its Roth status. For a full walkthrough of how this works, see our Rollover IRA guide. The 5-year clock for the earnings rule uses your Roth IRA's clock, not the Roth 401(k) clock. If your Roth IRA is older, that's fine. If your Roth 401(k) is older but you never had a Roth IRA before, the 5-year period starts when the money arrives in the Roth IRA.

Traditional IRA to Roth IRA (Conversion)

Covered above in the Roth Conversions section. The converted amount is taxable income in the year of conversion. Each conversion starts its own 5-year penalty clock.

The 60-Day Rollover Rule

Same as with Traditional IRAs. If you receive a distribution personally, you have 60 days to deposit it into another Roth IRA. Miss the deadline and the earnings portion becomes taxable (contributions are still tax-free since you already paid tax on them).

You're limited to one 60-day rollover per 12-month period across all your IRAs. Direct transfers don't count toward this limit. Why the 60-day rule is almost never worth the risk →

Common Mistakes

These aren't edge cases. These are the mistakes that come up repeatedly.

Thinking All Roth Withdrawals Are Tax-Free

Contributions, yes. Always. But earnings are only tax-free if the distribution is qualified. The 5-year rule exists. Age 59½ matters. People hear "Roth equals tax-free" and assume they can pull everything out whenever they want with no consequences. They can't.

Confusing the Two 5-Year Rules

The earnings clock and the conversion clock are separate. One is a lifetime clock that starts with your first-ever Roth contribution. The other restarts with each conversion. Mixing them up leads to unexpected penalties.

Contributing Over the Income Limit

If your MAGI exceeds the phase-out range, you can't contribute directly to a Roth IRA. Contribute anyway and you owe the 6% excess contribution penalty for every year the excess stays in the account. If your income varies year to year, check your eligibility before contributing.

Ignoring the Pro-Rata Rule on Backdoor Roths

You contribute to a non-deductible Traditional IRA and convert to a Roth. Clean and simple, right? Not if you have $200,000 in a rollover IRA from your old 401(k). The IRS aggregates all your Traditional IRA balances. Your "tax-free" conversion just became mostly taxable. How this catches people every year →

Not Starting the 5-Year Clock Early

Opening a Roth IRA with even $50 starts the 5-year clock. Some people wait until they have "enough" to make it worthwhile. Meanwhile, the clock isn't running. Five years later they wish they'd started sooner.

Forgetting That Conversions Have Separate Clocks

You converted in 2024 and again in 2026. Two separate 5-year clocks. If you're under 59½ and withdraw converted money, the IRS applies the penalty based on the specific conversion's clock, not when you first opened your Roth. First-in, first-out.

Not Naming (or Updating) Beneficiaries

The beneficiary designation on the account overrides your will. Check it after every major life event — divorce, remarriage, the birth of a child. The custodian has whoever you listed. That's who gets the money. Why people keep putting this off →

Tools for Roth IRA Planning

Running the Backdoor Roth? Need to fix an excess contribution? Wondering how the pro-rata rule affects your conversion? These tools walk you through it.

All tools include step-by-step explanations. See pricing →

Frequently Asked Questions

Can I have both a Roth IRA and a Traditional IRA?

Yes. You can contribute to both in the same year. The combined total across both accounts can't exceed $7,500 ($8,600 if you're 50+) for 2026.

Can I have a Roth IRA and a Roth 401(k)?

Yes. Different accounts with different limits. You can max out both. The Roth 401(k) has its own contribution limit ($24,500 for 2026, plus catch-up if eligible). The Roth IRA limit ($7,500) is separate.

What happens if my income goes over the limit after I contribute?

If you contribute to a Roth IRA and your MAGI ends up above the phase-out range, you have an excess contribution. You can fix it by withdrawing the excess (plus any earnings on it) before the tax filing deadline. Or you can recharacterize the contribution as a Traditional IRA contribution. Or you can apply it to the following year if you're eligible then.

Can I withdraw my contributions at any time?

Yes. Roth IRA contributions can be withdrawn at any time, for any reason, with no tax and no penalty. This is the fundamental flexibility advantage of a Roth. You already paid tax on that money. Note that this applies to contributions only — earnings and conversion amounts have different rules.

What's the Backdoor Roth IRA?

It's a two-step strategy for people whose income exceeds the Roth IRA contribution limits. You contribute to a non-deductible Traditional IRA, then convert it to a Roth IRA. The conversion is a taxable event, but if the contribution was non-deductible and there are minimal earnings, the tax bill is small. The pro-rata rule is the main complication — if you have other pre-tax IRA balances, those get factored into the tax calculation.

Is there a minimum amount to open a Roth IRA?

The IRS doesn't set one. Individual custodians might. Many brokerages let you open with $0 and contribute any amount.

What investments can I hold in a Roth IRA?

Same as a Traditional IRA. Stocks, bonds, mutual funds, ETFs, CDs, money market funds. You cannot hold life insurance, collectibles (art, antiques, gems, most coins), or S corporation stock directly.

Do I have to take RMDs from a Roth IRA?

No. There are no Required Minimum Distributions from a Roth IRA during your lifetime. The money can grow tax-free indefinitely. This is one of the key advantages over a Traditional IRA.

What happens to my Roth IRA when I die?

It passes to your designated beneficiaries. A spouse beneficiary can roll it into their own Roth IRA and continue with no RMDs. Most non-spouse beneficiaries must empty the account within 10 years under the SECURE Act's 10-year rule. The distributions are generally tax-free as long as the original owner's 5-year rule was satisfied. See our Inherited IRA guide for the full beneficiary rules.

Is a Roth IRA better than a Traditional IRA?

It depends on your current tax rate versus your expected tax rate in retirement. If you expect to be in the same or higher bracket later, the Roth wins because you're locking in today's rate. If you're in a high bracket now and expect a lower one in retirement, the Traditional IRA's upfront deduction is more valuable. There's no universal answer. We built a free comparison tool that runs the math for your specific situation: Roth vs. Traditional Comparison Tool →

Can I convert my Traditional IRA to a Roth after retirement?

Yes. There's no age limit and no employment requirement for conversions. Many people do their largest conversions in the early years of retirement before Social Security and RMDs push their income back up. The converted amount is taxable in the year you convert.

What's the difference between a Roth IRA and a Roth 401(k)?

The Roth 401(k) is employer-sponsored with higher contribution limits, no income restrictions, and required minimum distributions (unless rolled into a Roth IRA). The Roth IRA is individual, has income limits, lower contribution limits, but no RMDs and more withdrawal flexibility. Many people use both.

Related Knowledge Blasts

Short, plain-English breakdowns of the rules behind this guide:

- The Roth IRA 5-Year Rule — The Only Explanation You'll Ever Need →

- Roth 5-Year Rule Confusion →

- When a Backdoor Roth Works on Paper but Fails on the Tax Return →

- The Pro-Rata Rule in Roth and Traditional IRAs — Why It Ruins "Clean" Moves →

- Roth Conversion vs. Backdoor Roth: Why People Keep Mixing These Up →

- Excess Contribution Removal — What to Do Before the Deadline →

- Recharacterizations Explained →

- Beneficiary Designations — The Year-End Task People Avoid Until It's Too Late →

Education-only disclaimer

This guide is for general education and information only. It does not provide individualized investment, tax, or legal advice, and does not establish a client relationship with any firm or individual. Always consult your own tax professional, financial advisor, or legal counsel before making decisions about your accounts, investments, or retirement strategy.

Get the retirement rule mistakes most people learn too late

Daily: one retirement rule trap, why it happens, and the fix. Everyday-language IRS rule breakdowns from an 8-year Schwab/TD Ameritrade veteran. Free.

Join the Rundown — Free